> SMM Cold Rolling Production Schedule: Steel Mills Report Good Order Intake, October Cold Rolling Production Schedule Increases Slightly

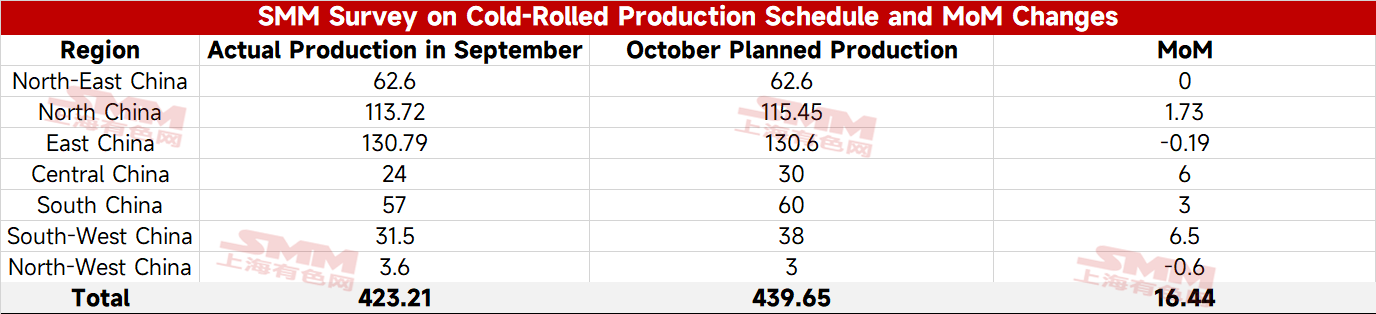

According to the latest SMM tracking, 31 mainstream steel mills plan to produce a total of 4.3965 million mt of cold-rolled commercial steel in October, up 164,400 mt MoM from the actual production in September, an increase of 3.9%.

On a daily average basis, October has one more day than September. The daily average production schedule for cold-rolled commercial steel in October is 141,800 mt, up 0.5% MoM from the daily average actual production in September.

> SMM HRC Production Schedule: October HRC Production Schedule Up 3.3% MoM, Daily Average Down 0.1% MoM

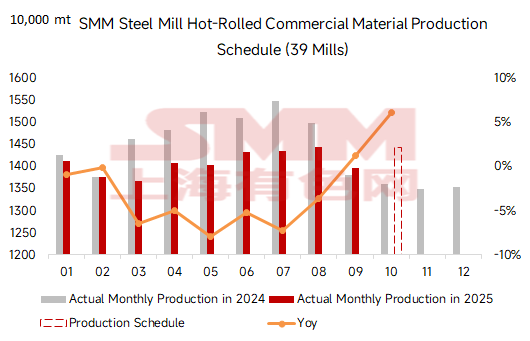

According to the latest SMM tracking, the total planned volume of HRC commercial material from 39 mainstream steel mills in October is 14.417 million mt, an increase of 455,300 mt compared to the actual HRC commercial material production in September, up 3.3% MoM.

On a daily average basis, October has one more day than September. The daily average HRC commercial material production schedule for October is 465,100 mt, down 0.1% MoM compared to the daily average actual production in September.

In October, steel mills in multiple regions including Northeast China, North China, East China, South China, and the western part of the country completed maintenance and resumed production. Additionally, according to SMM, the profitability and order situation for sheets & plates at most steel mills are currently better than those for building materials, prompting some mills to appropriately increase production of sheets & plates. Under these combined effects, the total production schedule for hot-rolled products at steel mills in October increased by 455,300 mt MoM. Since October has more days than September, the daily average production schedule for hot-rolled products at steel mills in October remained basically stable MoM.

Summary: The production schedule for hot-rolled commercial steel from steel mills in October increased by 3.3% MoM compared to September. However, as October has more days than September, the daily average production schedule for hot-rolled products in October actually decreased slightly by 0.1% MoM compared to the actual production in the previous month.

Looking ahead, some steel mills are expected to resume production in October after completing maintenance, while newly commissioned mills are increasing their market supply. Hot-rolled coil supply is anticipated to increase MoM. On the demand side, entering October, construction and infrastructure projects are expected to improve, while manufacturing performance may vary. Overall demand remains resilient and is projected to increase slightly compared to September. In the home appliance sector, according to the latest production schedule report for three major white goods released by ChinaIOL, the total production schedule for air conditioners, refrigerators, and washing machines in October 2025 is 29.24 million units, down 9.9% YoY. In the automotive industry, the fourth batch of trade-in subsidy funds is scheduled for distribution in October, which is expected to boost car purchase demand. Additionally, the NEV purchase tax exemption policy is set to expire at the end of December this year, potentially leading to front-loaded demand release.

During the National Day holiday, hot-rolled coil inventory accumulated significantly. Coupled with prices retreating after a rapid rise post-holiday, end-user procurement has turned cautious, and market sentiment remains weak. The focus is on the inflection point of inventory reduction. If destocking progresses slowly amid high supply, it will weigh on hot-rolled coil prices.

In other aspects, from a macro perspective, October still holds potential for a US Fed interest rate cut and important domestic meetings related to the 15th Five-Year Plan. Macro expectations are likely to intensify in the latter part of the month. On the cost side, hot metal production remains at a relatively high level, and raw material markets are subject to speculative factors, providing temporary cost support without significant risks. Recent escalation in Sino-US trade friction continues to suppress hot-rolled coil prices in the short term. Overall, the accumulation of supply-demand imbalance in hot-rolled coils remains limited for now. Subsequent inventory reduction will be key. Considering macro and cost support, the room for further price corrections in October is relatively limited.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)